When it comes to the choice between a Business Line of Credit and a Small Business Loan, important decisions need to be made. This comparison delves into the nuances of each option, shedding light on their differences and similarities.

Exploring the intricacies of business financing is crucial for any entrepreneur looking to make informed choices for their financial needs.

Introduction to Business Line of Credit and Small Business Loan

When it comes to financing options for small businesses, two common choices are business lines of credit and small business loans. Understanding the differences between these two can help business owners make informed decisions regarding their financial needs.

Business Line of Credit

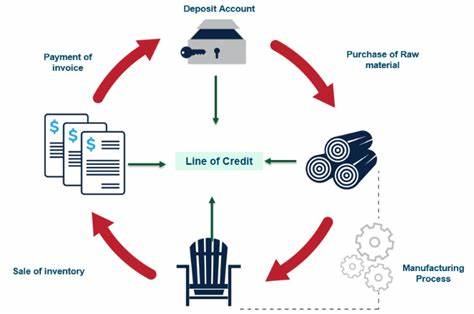

A business line of credit is a flexible form of financing that allows businesses to borrow funds up to a predetermined limit. Similar to a credit card, business owners can access funds as needed and only pay interest on the amount borrowed.

This type of credit is revolving, meaning that as the business repays the borrowed amount, the credit line is replenished, making it a continuous source of funding for ongoing expenses.

Small Business Loan

On the other hand, a small business loan is a lump sum of money borrowed from a lender with a fixed repayment schedule. The borrowed amount is typically used for specific purposes such as purchasing equipment, expanding operations, or covering one-time expenses.

Small business loans usually have a fixed interest rate and set repayment terms, providing a structured approach to borrowing.

Main Differences

- A business line of credit offers flexibility in borrowing and repayment, while a small business loan provides a lump sum amount with fixed terms.

- Business lines of credit are ideal for managing cash flow and covering ongoing expenses, whereas small business loans are better suited for one-time investments or purchases.

- Interest rates for business lines of credit may vary based on the amount borrowed and creditworthiness, whereas small business loans often have fixed interest rates.

- Business lines of credit can be continuously accessed as long as the credit limit is not exceeded, while small business loans require a new application and approval process for additional funds.

Purpose and Usage

When it comes to the purpose and usage of a business line of credit versus a small business loan, there are distinct scenarios where each option shines. Let's explore the common use cases for a business line of credit, examples of when a small business loan may be more suitable, and compare the flexibility in usage between the two.

Common Use Cases for a Business Line of Credit

A business line of credit is often used for managing cash flow fluctuations, covering short-term expenses, or seizing growth opportunities. It provides businesses with the flexibility to borrow funds as needed, up to a predetermined credit limit. Common use cases for a business line of credit include:

- Seasonal inventory purchases

- Managing payroll during slow months

- Investing in marketing campaigns

- Addressing unexpected expenses

When a Small Business Loan is More Suitable

While a business line of credit offers flexibility, there are situations where a small business loan may be a more appropriate choice. Small business loans are typically used for larger, one-time investments or long-term financing needs. Examples of when a small business loan may be more suitable include:

- Expanding to a new location

- Purchasing expensive equipment

- Funding a major renovation

- Acquiring another business

Flexibility in Usage Comparison

In terms of flexibility in usage, a business line of credit allows businesses to access funds on an as-needed basis, similar to a credit card. This means they only pay interest on the amount they borrow. On the other hand, a small business loan provides a lump sum upfront, which is repaid over a fixed term with regular payments.

The choice between a line of credit and a small business loan ultimately depends on the specific financial needs and goals of the business.

Qualification Requirements and Approval Process

When it comes to obtaining financial assistance for your business, understanding the qualification requirements and approval process for a business line of credit and a small business loan is crucial. Let's delve into the typical criteria and steps involved in securing these forms of funding.

Business Line of Credit

A business line of credit usually requires the following eligibility criteria:

- Minimum time in business (typically 6 months to 2 years)

- Minimum annual revenue (varies depending on the lender)

- Good personal and business credit scores

- Positive cash flow and profitability

Small Business Loan

Obtaining a small business loan involves the following typical approval process:

- Submit a loan application with detailed business and personal financial information

- Provide business plan, financial projections, and collateral (for secured loans)

- Undergo credit check and assessment of creditworthiness

- Wait for lender's approval decision, which can take a few days to weeks

Both options have specific documentation and credit score requirements. Business lines of credit typically demand a credit score of 600 or above, while small business loans may require a higher score, usually 640 or more. Additionally, small business loans often necessitate collateral to secure the loan, whereas business lines of credit are usually unsecured, relying more on creditworthiness and revenue history.

It is essential to understand these distinctions to determine which financing option aligns best with your business needs and financial situation.

Interest Rates and Fees

When considering business financing options, it is crucial to understand the different interest rate structures and fees associated with business lines of credit and small business loans. These factors can significantly impact the overall cost of borrowing and affect the total amount paid back.

Interest Rate Structures

- Business Line of Credit: Interest rates for business lines of credit are typically variable, meaning they can fluctuate based on market conditions. The rates are often tied to a benchmark rate, such as the prime rate, plus a certain percentage determined by the lender.

- Small Business Loan: Small business loans usually come with fixed interest rates, meaning the rate remains the same throughout the term of the loan. This provides predictability for monthly payments.

Fees Impact

- Business Line of Credit: In addition to interest charges, business lines of credit may come with fees such as maintenance fees, draw fees, or early closure fees. These fees can add to the overall cost of borrowing.

- Small Business Loan: Small business loans may also have origination fees, application fees, or prepayment penalties. It is essential to factor in these fees when calculating the total cost of the loan.

Understanding the interest rate structures and fees associated with business financing can help business owners make informed decisions and choose the most cost-effective option for their needs.

Repayment Terms and Flexibility

When it comes to comparing a business line of credit and a small business loan, understanding the repayment terms and flexibility is crucial for making an informed decision.

Business Line of Credit

- A business line of credit typically offers more flexible repayment terms compared to a traditional loan. Instead of making fixed monthly payments, you only pay interest on the amount you use.

- Repayment schedules are often open-ended, allowing you to borrow, repay, and borrow again without going through a new approval process each time.

- Minimum monthly payments are usually required, but you have the flexibility to repay the full amount at any time without penalty.

Small Business Loan

- Small business loans generally come with fixed repayment schedules, requiring you to make regular monthly payments that include both principal and interest.

- The repayment terms are predetermined and may range from a few months to several years, depending on the loan amount and terms.

- While some lenders offer flexibility in terms of adjusting payment schedules in case of financial hardship, the overall structure remains more rigid compared to a line of credit.

Impact on Cash Flow

Repayment terms and flexibility play a significant role in the cash flow management of a business. A business line of credit allows for more control over when and how much you repay, providing better cash flow management during lean months.

On the other hand, a small business loan with fixed monthly payments can put a strain on cash flow, especially if business revenues fluctuate. It's essential to consider your cash flow needs and financial stability when choosing between a line of credit and a traditional loan.

Impact on Credit Score and Financial Health

Utilizing a business line of credit or taking out a small business loan can have a significant impact on a business owner's credit score and overall financial health. It is essential to understand how these financial decisions can affect your business and personal finances in the long run.

Impact of Business Line of Credit

A business line of credit can positively impact your credit score if managed responsibly. Timely payments and keeping credit utilization low can help improve your credit score over time. However, maxing out your credit line or missing payments can have a negative impact on your credit score.

It is crucial to use the line of credit wisely and make payments on time to maintain a healthy financial profile.

Long-Term Implications of Small Business Loans

Taking out a small business loan can have long-term financial implications for your business. While it can provide the necessary funds to grow your business, it also means taking on debt that needs to be repaid with interest. Failure to repay the loan on time can damage your credit score and financial health.

It is important to consider the impact of the loan on your cash flow and financial stability before taking on additional debt.

Tips for Managing Your Credit and Financial Health

- Monitor your credit score regularly to track any changes and address any issues promptly.

- Make timely payments on your business line of credit or small business loan to maintain a positive credit history.

- Keep your credit utilization low to avoid maxing out your credit line and damaging your credit score.

- Create a budget and financial plan to ensure you can afford the monthly payments on your loan or line of credit.

- Seek financial advice from a professional if you are struggling to manage your credit and debt effectively.

Wrap-Up

As we wrap up our exploration of Comparing a Business Line of Credit vs Small Business Loan, it becomes evident that understanding the intricacies of each option is key to making the right financial decisions for your business.

Q&A

Can I use a business line of credit for long-term investments?

A business line of credit is typically used for short-term financing needs like managing cash flow, while a small business loan might be more suitable for long-term investments.

What are the typical documentation requirements for a small business loan?

Small business loans usually require detailed business plans, financial statements, and information about the purpose of the loan.

How does repayment flexibility differ between a line of credit and a small business loan?

A business line of credit offers more flexibility in repayment schedules compared to the more structured repayment terms of a small business loan.

Will taking out a small business loan impact my personal credit score?

Generally, taking out a small business loan will impact your business's credit score rather than your personal credit score, as long as you keep your business finances separate.

{kind=link}